5th March 2012 – Please note the initial review below was for a rate at 3.40%-3.60% over the 90 day BBSW. This has since been increased to and indicative rate of 3.80%-4.00% over the 90 day BBSW and we now feel this offer is relatively attractive to investors.

Due to timescales, we have maintained the initial analysis below and provided an update at the end of this review.

Analysis from 1st March 2012

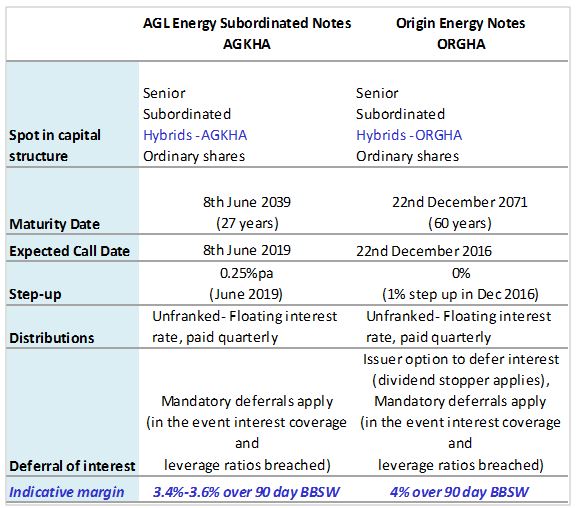

AGL Energy has just announced the launch of a new income offer: AGL Energy Subordinated Notes.The first round of access is through a broker firm allocation, prior to a shareholder offer and listing on the ASX in April.

The Notes will pay a quarterly coupon of 3.40%-3.60% over the 90 day bank bill swap rate (BBSW), which is 4.45% as of 27th February, with an initial indicative income of 7.85%-8.05%pa. The first quarter’s income is due to be set on date of issue and are expected to redeem 8th June 2019*. The Notes will be tradable on the ASX.

This issue will be used primarily to assist in funding AGL’s purchase of the Loy Yang A power station and adjacent coal mine.

Although this is a 27 year bond, it is expected that the issue will be repaid at the first opportunity in June 2019. Professional market participants expect that this issue will be redeemed in 2019 as the Notes would be treated as debt by credit ratings agencies after this date. The Notes are expected to be treated as equity for the first 7 years which assists AGL in lowering their overall funding costs.

Our view on AGL Energy Notes

Having discussed this issue with a number of analysts, overall views on AGKHA are split. Some have derided the lower margin of 3.4% to 3.6% above the BBSW, making comparisons to the recent Origin Energy Issue at 4% over the 90 day BBSW. They are of the opinion that the return does not compensate investors enough.

Others have the view that AGL Energy’s defensive income stream and high interest cover ratio make this Note a safer security than Origin, pointing to the relatively low cost of senior debt as an indicator of where these Notes should be priced.

Based on these divergent views, we are finding it difficult to assess the appropriate margin for these Notes. The most comparable hybrids on issue are the Origin Energy Notes (ORGHA) which were issued in December, but Origin has a portfolio of capital intensive, immature energy projects. The market is right in demanding a higher rate of return from Origin’s Notes since they have lower interest cover and higher cash flow requirements for its Queensland LNG project.

The question is how much of a margin is fair?

With ORGHA currently trading at just over $102, the yield for new investors buying on market, equates to around 3.9%pa + BBSW (incorporates an investor only receiving $100 back at the expected call date in Dec 2016 and an accrued dividend of $1.50). The likely 3.4% +BBSW margin offered by AGL Energy Notes does not seem unreasonable in contrast given AGL’s balance sheet. Indeed, some analysts point to the institutional bond (CDS) market where AGL trades at around 0.2%pa more than Woolworths and at a narrower margin than the banks. Having said that we are also of the view that Origin Energy Notes are slightly overvalued so where AGL should actually sit is difficult to assess. One key benefit in this issue is that we are following $5 Billion of new issues to a market that only had $20 Billion of listed hybrids. With the expectation that there are more to come, AGL may have to dig a little deeper than the lower end of 3.4% margin.

Overall, we feel that this Note is priced without much capital upside for the investor. In its favour, we feel it is unlikely that AGL will raise much beyond their stated objective of $650 Million and with only $50 Million available through the customer and shareholder offer, there is likely to be some support after its initial listing on the ASX.

Key Points

- Indicative floating yield of 7.85%-8.05% (3.40%-3.60% over 90 day BBSW of 4.45%).

- Interest protected – Although the issue terms allow for deferral of ORGHA interest payments at AGL’s discretion for up to 5 years, investors are protected by the dividend stopper which prevents AGL equity investors from receiving the payment of ordinary dividends if the Notes do not receive their interest payment.

- Mandatory deferral of interest – If AGL’s ability to service debt and overall level of debt (Interest Cover Ratio and Leverage Ratio) becomes problematic, interest on the Notes is deferred for up to 5 years.

- Financial Strength – AGKHA provides investors exposure to one of the larger companies listed on the ASX and a market cap of over $6bn.

- Credit Rating – It should be noted that AGKHA has considerable financial incentives to maintain a high credit rating. Lower credit ratings lead to higher cost of capital on further issues and we note that the supply of energy contracts are likely to be dependent on maintaining a high rating. An important aspect of this issue is the expectation that credit ratings houses only provide equity credit for the first 7 years, after which it would be considered to be debt and likely to impact on AGL’s credit rating. We therefore expect this issue to be repaid in 7 years.

Update 05/03/12 – Indicative rate increased to 3.80%-4.00% over the BBSW

Since we initially reviewed this product, AGL have increased the indicative rate to 3.80%-4.00% over the 90 day BBSW. We suspect that the flood of recent hybrids has been to the detriment of AGL Notes, forcing them to pay a more competitive rate as investors become jaded to the endless stream of hybrids being offered.

We are surprised to see such a large step up in the rate offered and is either indicative of low demand (remember we only expect them to take just over the $650 Million being offered) or is a change in tactics to try an prise more money from Notes investors and less from the rights issue. Relative to the demand we say from direct investors in the last week, we suspect this is due to the over-supply of $5 Billion of new issues in 2 weeks and expect this to come in at 3.8% over the 90 day BBSW. As a result, we feel this provides investors with some upside.

Best regards

Sulieman Ravell

Wealth Focus Pty Ltd

Comment: