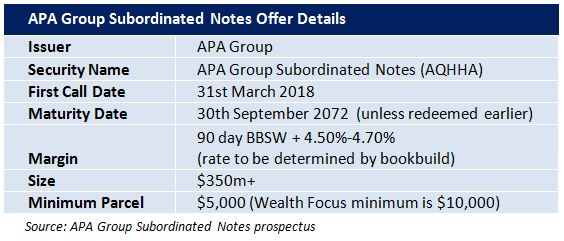

APA Group has just announced the launch of a new income offer: APA Group Subordinated Notes.The first round of access is through a broker firm allocation, prior to shareholder offer and listing in September.

The Bonds will pay a quarterly coupon of 4.50%-4.70% over the 90 day bank bill swap rate (BBSW), 3.63% as of 8th August, with an initial indicative rate of 8.13%-8.23%pa. (The first quarter’s pricing is due to be set on date of issue) and are expected to redeem 31st March 2018*. The Notes will be tradable on the ASX.

This issue will be used primarily to assist in funding APA Group’s purchase of Hastings Diversified Utilities Fund.

Although this is a 60 year Note, it is expected that the issue will be repaid at the first opportunity in March 2018. We feel it unlikely the issue would continue after this date as the Notes would expected to then be treated as debt by credit ratings agency, S&P, if it is not redeemed. Until March 2018, it is expected that around 50% of this debt is considered equity by ratings companies, enhancing their rating and lowering the overall cost of borrowing in the institutional markets.This issue will be used primarily to assist in funding APA Group’s anticipated purchase of Hastings Diversified Utilities Fund.

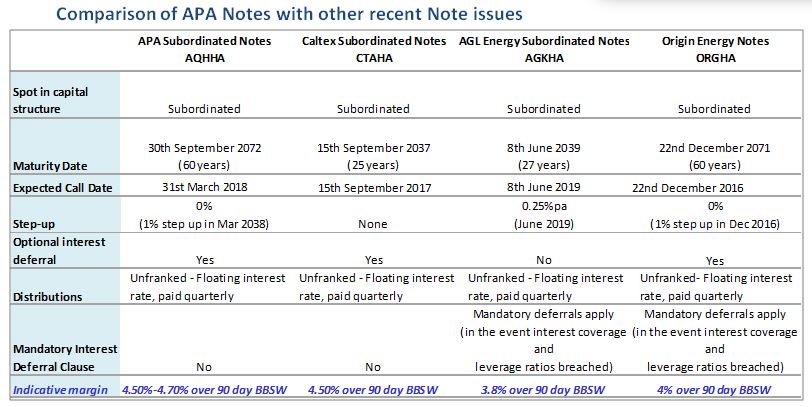

Comparative Securities

Interestingly enough, we feel the closest comparable is Caltex Subordinated Notes which was launched last week. This was quickly closed two days later with large scale backs for a $300 Million issue which was increased to $525 Million (inclusive of shareholder & general offer).

We note that Caltex & APA OTC bonds issued in the institutional market trade at similar spreads to each other and therefore expect a similar demand for APA Group Subordinated Notes.

Investors looking to make comparisons with AGL and Origin Energy Subordinated Notes may be re-assured by them currently trading above face value.

Comparison of APA Notes with other recent Note issues

Key Points

- Indicative floating yield of 8.13%-8.23% provides investors the opportunity to take advantage of historically high hybrid margins.

- Interest protected – Although the issue terms allow APA Group to defer interest payments at their discretion, investors are protected by the dividend stopper requiring non payment of ordinary dividends.

- Financial Strength – AQHHA provides investors exposure to an ASX 100 listed company with a market cap of over $3bn.

- Redemption highly likely in 5 years – although AQHHA has a 60 year maturity, we think APA will redeem at the first redemption date in March 2018. Two major incentives for redemption include the potential for reputational damage and the loss of equity credit as applied by ratings agencies. Not paying in 6 years is likely to lead to an increased cost of funding on future debt issues.

Our View

The current demand for fixed income investments means that AQHHA is likely to issue at 4.50% over the BBSW, an attractive premium in an absolute sense when compared to recent issues such as AGL Subordinated Notes currently trading at around 3.75% over the 90 day BBSW and Origin Energy Subordinated Notes, currently trading at around 3.85% over the 90 day BBSW.

In light of last week’s Caltex issue, we think the demand will be very high for AQHHA and is likely to be reflected in a small trading premium on listing.

Overall we feel this issue is attractive but investors should be aware that the higher income reflects the added risk. Our advice is to research APA and their asset pool before investing in this issue.

Note: APA Group Notes will be listed on the ASX and as such the price of the Note’s will be subject to market movements. Investor’s selling on market may receive a price lower (or higher) than the issue price.

Investors looking for an allocation can contact us on 1300 559 869

We encourage you to view our online presentation An Introduction to Fixed Income

Best regards

Sulieman Ravell

Wealth Focus Pty Ltd

Comment: