CBA has just announced the launch of a new income offer: CommBank Perls 8 Capital Notes. The first round of access is through a broker firm allocation, prior to shareholder offer and listing in March. Note: There is no Customer or General Offer

The Notes will pay a quarterly coupon of 5.2%-5.35% (rate determined by the bookbuild) over the 90 day bank bill swap rate (BBSW), which was 2.29% as of 16th February, with an initial indicative rate of 7.49%-7.64%pa. (The first pricing is due to be set on date of issue) The Notes are expected to redeem on the 15th October 2021** and will be tradable on the ASX.

** It is expected that the issue will be repaid at the first opportunity in October 2021 with a scheduled conversion in 2023 (subject to mandatory conditions not being breached).

Our analysis

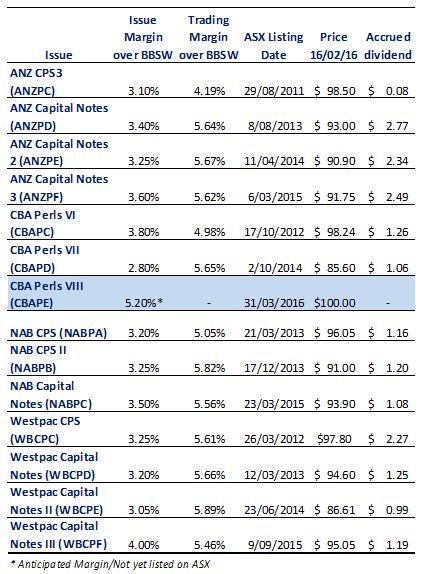

There is now an established secondary market for the newer style bank hybrids from the Big 4 banks, and investors could be forgiven for focusing on the historically high yield being offered by CBA. At a margin of 5.2% over the Bank Bill Swap Rate (BBSW), currently 2.29%pa, that is considerably higher than the next highest issue margin from Westpac in 2015 at 4% over BBSW.

We view ANZ Capital Notes (ANZPD), NAB CPS II (NABPB), and Westpac Capital Notes 2 (WBCPE) as the closest comparables, maturing in Dec 2020 – March 2022.

CBAPC, CBAPD, CBABE, NABPA, NABPB, WBCP, WBCPE & WBCPF structures offer a margin over the 90 day BBSW, ANZPC, ANZPD, ANZPE, and WBCPD offer a margin over the 180 day BBSW.

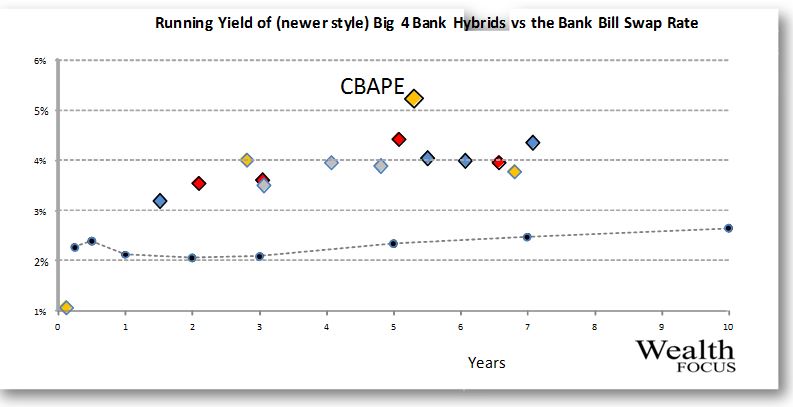

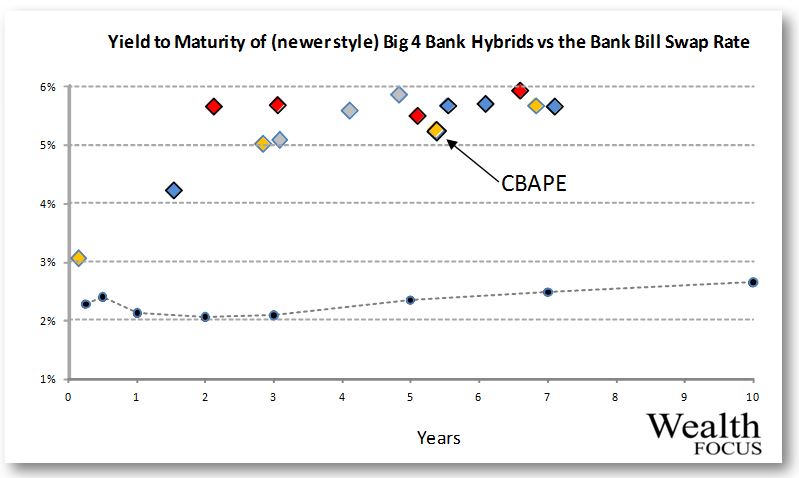

An anomaly currently exists within the market, with hybrids seemingly trading in line with the running yields, rather than the Yield To Maturity (YTM). This indicates that the market’s expectation is either that the banks are unlikely to repay their debt at the anticipated call/repayment date or that it is unable to correctly assess the margin to maturity (running yield + capital gain when repaid at face value).

It is our view that the secondary market is inefficient, presenting an opportunity for savy investors who are able to correctly assess the additional benefit of a potential capital gain when held to maturity. The banks’ overall reliance on debt markets provides a strong impetus for them to repay at the first opportunity and we view the risks of not repaying as relatively low.

Investors should feel re-assured by CBA opting to call Perls III in April by issuing a replacement when spreads in the hybrid market have blown out to such a wide margin. By replacing CBA Perls III (PCAPA), at 1.05% over BBSW (step up to 2.05% post April), with a new issue costing CBA 5.2% over BBSW, the increase in cost of funding is 3.15%pa and demonstrates “the stick” of reputational risk, ensuring banks repay at the first opportunity to avoid increased cost of further borrowing.

Non-viability Clause, Capital Trigger Event and Inability Event

Investors who are familiar with the new style hybrids we have seen over the last couple of years will be very aware of these clauses.

It is perhaps useful to understand that these clauses are as a result of APRA requiring further reassurance that in another GFC event, if required , hybrids would convert to ordinary equity, thereby reducing the bank’s debt costs and protecting deposit holders.

Now that banks have to hold a higher level of capital and a better quality loan book, it seems unlikely that any of these conditions would be breached, however, investors would do well to consider the increased disclosure and warnings within each prospectus over the last couple of years.

For those unfamiliar with the conditions, new hybrids now contain non-viability and capital trigger clauses that should the bank’s Tier 1 Capital Ratio fall below 5.125%, or APRA views the bank as non-viable without an injection of capital, the hybrids would automatically convert to ordinary shares.

We have also seen a gradual introduction of an Inability Event Clause added which states that in the event that the issuer is unable to issue further ordinary shares, ie the company has ceased trading, a Capital Trigger Event or Non-Viability Event, hybrid note holders lose their investment.

This is extremely unlikely, but investors would do well to remember the increase in yield offered carries additional risk.

Our View on CBA Perls 8

As per our previous reviews, we maintain our concerns over the non-viability clauses within new style hybrids, but investors looking to switch equity allocation into a more stable alternative would do well to consider these newer style hybrids. (We do not consider hybrids a suitable alternative for fixed income/cash)

Term deposit yields have continued to fall over the last year and we anticipate the RBA is likely to cut them further again this year. This leaves investors with the dilemma of reducing capital or switching to higher risk assets to support their income needs.

The last 9 months has only served to demonstrate why investors need to look for alternatives to equities.

Our view is that relative to alternatives such as NABPB, investors should demand a premium of close to 5.9% over the BBSW and looks expensive if issued at a margin of 5.2%-5.35% (approx 3% overpriced). However, we note that the secondary market seems to more readily trade on the Running Yield, suggesting that CBA Perls VIII should trade at $108.

In short, we feel that at a margin of 5.2%-5.35% over BBSW, CBAPE is overpriced relative to the current yields available in the secondary market. By contrast, it would not surprise us to see this list and trade at a premium of 2-3%.

Other existing alternatives clearly offer better value but our gut feel is that it is likely to trade above the $100 issue price from day one and offer less volatility than the other hybrid alternatives.

Investors should also be aware that the primary role of Perls 8 is to refinance $1.1 Billion of Perls 3 and priority tends to be given to Perls 3 holders looking to roll their existing investments.

As a result, we expect that a considerable portion of the $1.25 Billion of CBAPA will roll into the new issue, leaving very little on the table for new investors.

Contact us if you would like an allocation to CBA Perls 8 or have an existing investment in CBA Perls 5 you would like to roll into the new issue.

Key features

- Indicative floating yield of 7.49-7.64%pa – based on current 90 BBSW of 2.29% and bookbuild margin range of 5.2-5.35%.

- Option to redeem at year 5 with scheduled conversion at year 7 -CBA has the option to convert in October 2021 or on any subsequent dividend payment date.

- Ordinary dividend restrictions -applies on the non payment of CBAPE dividends

- Automatic conversion under the Capital Trigger Event and Non-Viability

- Redemption highly likely in 5.5 years -although CBAPE has a 7.5 year maturity, its likely CBA will redeem/convert at the first call date in October 2021. Major incentives for redemption/conversion include the potential for reputational damage and risk of credit rating downgrade, leading to an increased cost of funding on future debt issues.

Note: CBA Perls 8 will be listed on the ASX and as such the price of the Note’s will be subject to market movements. Investors selling on market may receive a price lower (or higher) than the issue price.

Investors looking for an allocation can contact us on 1300 559 869

We encourage you to view our online presentation An Introduction to Fixed Income

Best regards

Sulieman Ravell

Wealth Focus Pty Ltd

Comments | Click to comment

Is there a cash redemption price for perles VIII other than the conversion to shares ??

Ross, 27 April, 2021

Yes, issuers typically offer to redeem at face value ($100 in this case)

Sulieman Ravell, 4 December, 2021

Comment: