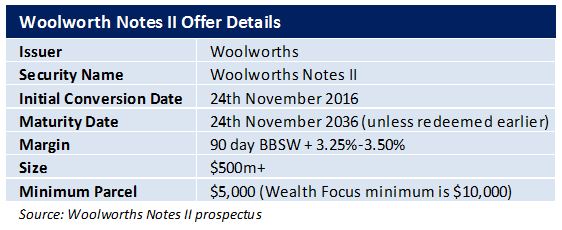

Woolworths has just announced the launch of a new income offer: Woolworths Notes II.The first round of access is through a broker firm allocation, prior to general offer and institutional offer before listing in November.

The Notes will pay a quarterly coupon at 3.25%-3.50% over the 90 day bank bill swap rate (BBSW), 4.76% as of 17th October, with an initial indicative rate of 8.01%-8.26%pa. (The first quarter’s pricing is due to be set on date of issue) and are expected to redeem 24th November 2016*. The bond will be tradable on the ASX.

This issue will be used as part of Woolworth’s ongoing capital management strategy and replace the $600 Million of Woolworths Notes (series 1) that were recently redeemed.

Although this is actually a 25 year bond, it is expected that the issue will be repaid at the first opportunity in November 2016. We feel it unlikely they would continue after this date as the interest rate steps up by a further 1%pa and the company would risk its reputation in the market, resulting in a higher cost of borrowing on future issues. An example of this is the Woolworths Notes (series 1) issue that would have stepped up to 3.1% over the BBSW had the Note been repaid earlier this year. Woolworths chose to repay this debt at considerable cost rather than damage its financial reputation. In addition to this, ratings agencies such as S&P structure their ratings in a way which encourages issuers to buy back their debt at the first call date (after 5 years in this case).

Attractive Pricing

In our opinion, the Notes look reasonably attractive on a number of measures;

- Woolworths Notes II compare favourably with other recent hybrid issues such as the ANZ CPS2 and CPS3, and although ANZ as a company is a higher rated issuer than Woolworths, a strong corporate such as Woolworths typically trades on tighter margins than major bank debt in the wholesale market.

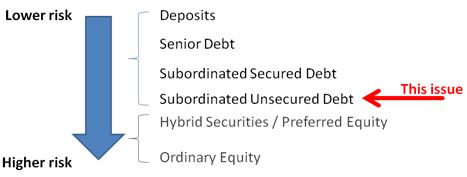

- Woolworths has an existing (wholesale) senior debt bond maturing on 22 May 2016 at a fixed rate of 5.7%pa (equivalent of 1.15% over the 90 day BBSW). Whilst this is senior to this issue, the liquidity provided by the ASX is an attractive feature and suggests there should be strong institutional demand.

Woolworths has a relatively low level of debt and high operating margins. At 3.25% over the BBSW and no franking credit, the relatively high income level is also likely to be attractive to overseas institutions who can’t benefit from franking.

As a result and assuming the share markets don’t drop off the cliff in the next few weeks, we would not be surprised to see a valuation in line with the bank issues such as ANZPA and trading excess of $103 a Note.

Note: Woolworths Notes II will be listed on the ASX and as such the price of the Bond’s will be subject to market movements. Investor’s selling on market may receive a price lower (or higher) than the issue price.

Best regards

Sulieman Ravell

Wealth Focus Pty Ltd

Comment: