Capital Protection – Reading between the lines

Increased volatility is bad news for CPPI / Threshold Management

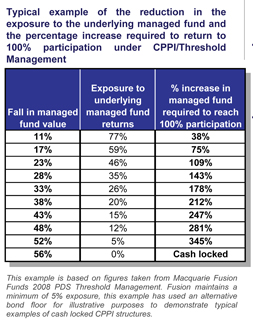

2008 saw many investors in CPPI products cash locked with no hope of getting back more than they had originally invested at the end of the investment. We consider why CPPI products are disadvantaged in a world of increasing volatility.

Investors using CPPI products such as Perpetual’s PPI Series have recently found themselves cash locked. ie in a falling market, once the investment has switched entirely to cash, they are no longer able to participate in the returns of the underlying managed fund. Those with 100% investment loans are now in a situation of having to continue their loan repayments with the knowledge that they will only ever get back what they borrowed at the end of the term.

The process of switching to cash as the investment falls in value and reinvesting in the managed fund as the investment rises in value means that even if a fund doesn’t become cash locked, investors such as those using Macquarie’s Fusion Funds or Perpetual’s Protected Investment Series can quite easily find themselves in a situation where the need the underlying managed fund to rise by 200%-300% before they are fully invested again. Furthermore, the increased volatility we are now witnessing in the markets mean that these products are much more likely to hit sell trigger points as the managed fund fluctuates in value.

In Conclusion

Our house view is that Bond + Call structures & Axa’s Dynamic Hedging are a much more attractive proposition to investors than CPPI protection structures. The increased volatility in the markets coupled with the reduction in participation in the underlying managed fund means that there is an additional cost to simply being invested in cash. However, it would be wrong to dismiss these products altogether, in many cases they offer protection and availability of investment loans to managed funds that are generally not available elsewhere. Platinum’s range of funds are an example of funds that have faired reasonably well under this structure.

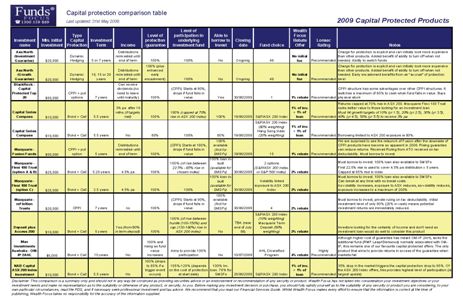

Of the capital protected products currently in the market, we currently favour the following:

Man Investment OM-IP 2AHL – This is the only product that doesn’t rely on the investment markets rising. AHL is a trend seeking strategy that profits from both rising and falling trends. The lack of exposure to RMF or Glenwood means this is not as attractive as past OM-IP offers, but still one of the best capital protected offers available.

NAB Principal Series ASX200 Index Investment – Has the highest level of participation in the ASX 200 Index, (currently indicating towards the upper end, 105%-120%). However, increased participation is as a result of lower protection levels.

Axa North Protected Investment Guarantee – this is a revolutionary product for those looking to invest in a managed fund with capital protection allowing you to benefit from 100% participation at all times, providing larger gains than CPPI structures. Downside is that early encashment after a fall in value is likely to return lower amounts than CPPI.

We have put together a comparison list of products in the market to enable investors to readily compare some of the offers currently available. Please click on the image below to download our end of tax year tables or via our latest offers page to view the most up to date version.

Click table to view

Comment: