ANZ Bank has just announced the launch of a new income offer: ANZ Capital Notes 3.The first round of access is through a broker firm allocation, prior to shareholder offer and listing in March.

The Notes will pay a semi annual coupon of 3.6%-3.8% (rate determined by the bookbuild) over the 180 day bank bill swap rate (BBSW), which was 2.69% as of the 23 January, with an initial indicative rate of 6.19%-6.39%pa. (The first pricing is due to be set on date of issue) The Notes are expected to redeem on the 24th March 2023* and will be tradable on the ASX.

It is expected that the issue will be repaid at the first opportunity in March 2023 with a scheduled conversion in 2025 (subject to mandatory conditions not being breached).

How does this compare?

The newer style hybrid market is now well established and there are a large number of newer style listed hybrids containing the additional clauses required to qualify them under APRA’s capital requirements for the banks.

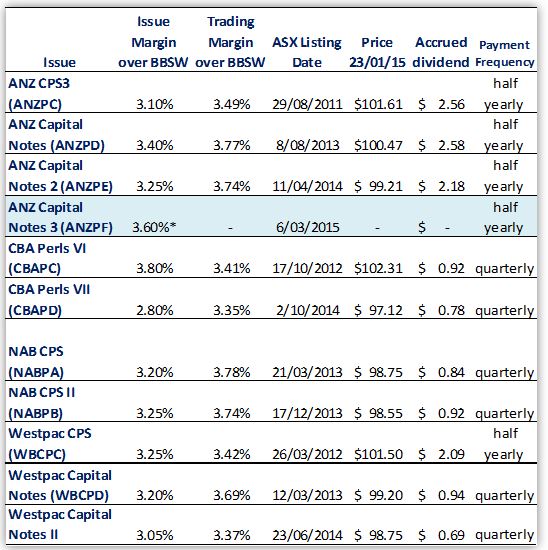

Investors looking for comparables would do well to consider issues such as CBA Perls (CBAPC & CBAPD), Westpac CPS (WBCPC) and Capital Notes (WBCPD & WBCPE), ANZ CPS3 (ANZPC) and ANZ Capital Notes (ANZPD & ANZPE), as well as NAB CPS (NABPA & NABPB).

The closest comparables are CBAPD and WBCPE, both issued in 2014, with a similar maturity profile.

A quick analysis

ANZPF’s closest comparables, CBAPD and WBCPE, currently trade at $97.12 (inc. $0.78 accrued dividend) and $98.75 (inc. $0.69 accrued dividend) respectively, with effective margin to expected maturity of 3.41%pa and 3.37%pa.

By contrast, ANZPE, the next closest comparable, trades at an effective margin of 3.74%pa over the BBSW with almost identical terms to ANZ’s latest issue.

The yields reflected are notional yields to maturity

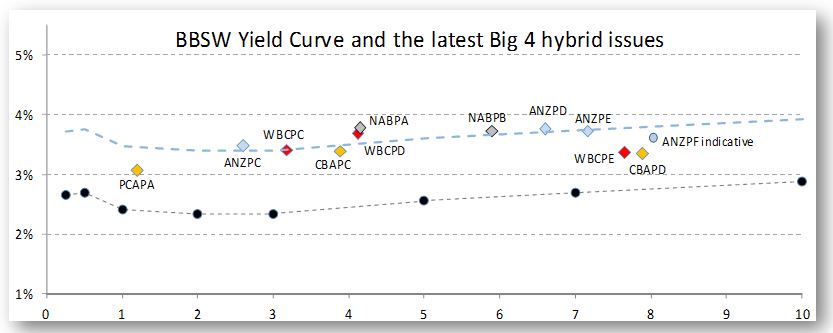

Using the Bank Bill Swap Rate (BBSW) yield curve as indicative of the additional premium investors should demand for the additional duration, we see fair value as the top of the range offered (3.8% over the BBSW).

Non-viability Clause, Capital Trigger Event and Inability Event

Investors should familiarise themselves with these clauses as we see these as some of the key risks of investing in newer style hybrids. These clauses are now well established within the market and have become accepted as a requirement in order to issue capital that conforms with APRA requirements.

In layman’s terms, should the bank fall on hard times, the hybrids convert to ordinary shares, likely leading to a loss in capital value and in some instances, if the issuer is unable to issue further ordinary shares at time of conversion, hybrid note holders lose their investment.

We acknowledge that this is extremely unlikely but reflects the increased risk we’ve seen added to hybrid issues over the last few years.

Our View

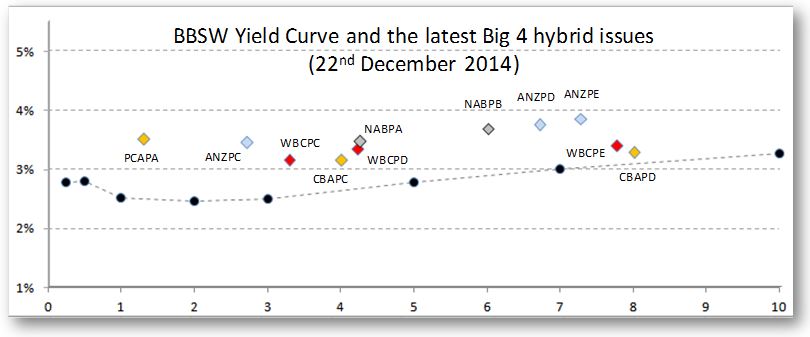

An anomaly currently exists in the hybrid market. Investors should expect to be rewarded with a higher return for a longer investment term, yet the last two issues from the Big 4 (WBCPE and CBAPD), continue to trade at a significantly lower margin than their shorter dated comparables.

This is perhaps indicative of investor’s views that the wide margins being offered are “too good to be true” and with the RBA anticipated to cut rates further, investors are ploughing in to longer term issues. We did also consider that maybe the market has priced in a new issue from ANZ and selling down existing ANZ hybrids, but this anomaly has existed for a prolonged period.

The yields reflected are notional yields to maturity

The increased volatility in the market over the last 6 months has once again placed a spotlight on equity returns with 10% swings seemingly becoming the norm. With the market anticipating a rate cut from the RBA, this issue will doubtlessly be oversubscribed at the bottom end of the range of 3.6% over the BBSW (indicative rate of 6.29%pa).

Relative to last year’s issues from Westpac (WBCPE) and CBA (CBAPD), this looks to be well priced, seemingly offering an additional 0.25% premium for a similar risk/term.

However, we think investors would be better placed to consider ANZPE as a comparable, which offers a yield to anticipated maturity of 3.74%pa. As a result, we would suggest 3.8% over the BBSW is a fair price.

What the brokers won’t tell you

NAB announced their intention to launch a new hybrid in an ASX release on the 15th December. We expect this will be announced over the next week or so and in light of ANZ’s issue will need to be a more compelling offer.

Our view is at 3.60% over the BBSW, there is not enough meat on the bone, sit tight and wait for NAB or place a bid via us at the higher margin of 3.8%.

Key features

- Indicative floating yield of 6.29%-6.49%pa – based on current 180 BBSW of 2.69% and bookbuild margin range of 3.60-3.80%. First payment due on 24th September 2015.

- Option to redeem at year 8 with scheduled conversion at year 10 –ANZ has the option to convert in March 2023 or on any subsequent dividend payment date.

- Ordinary dividend restrictions –applies on the non payment of ANZPF dividends

- Automatic conversion under the Capital Trigger Event and Non-Viability

- Redemption highly likely in 8 years –although ANZPF has a 10 year maturity, we think ANZ will redeem/convert at the first call date in March 2023. Major incentives for redemption/conversion include the potential for reputational damage and risk of credit rating downgrade, leading to an increased cost of funding on future debt issues.

Note: ANZ Capital Notes 3 will be listed on the ASX and as such the price of the Notes will be subject to market movements. Investor’s selling on market may receive a price lower (or higher) than the issue price.

Investors looking for an allocation can contact us on 1300 559 869

We encourage you to view our online presentation An Introduction to Fixed Income

Best regards

Sulieman Ravell

Wealth Focus Pty Ltd

Comment: