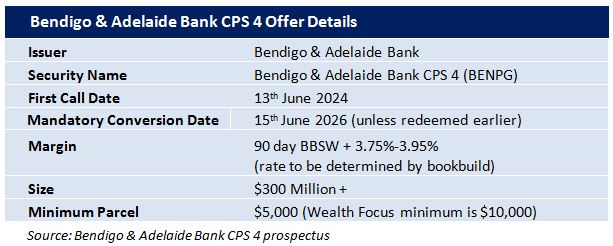

Bendigo & Adelaide Bank has just announced the launch of a new income offer: Bendigo & Adelaide Bank Convertible Preference Shares 4. The first round of access is through a broker firm allocation, prior to shareholder offer and listing in December.

Note: There is no Customer or General Offer

The Shares will pay a quarterly coupon of 3.75%-3.95% (rate determined by the bookbuild) over the 90 day bank bill swap rate (BBSW), which was 1.70% as of 16th October, with an initial indicative rate of 5.45%-5.65%pa. (The first pricing is due to be set on date of issue) The Shares are expected to redeem on the 13th June 2024** and will be tradable on the ASX.

** It is expected that the issue will be repaid at the first opportunity in June 2024 with a scheduled Conversion in 2026 (subject to mandatory conditions not being breached).

Our analysis

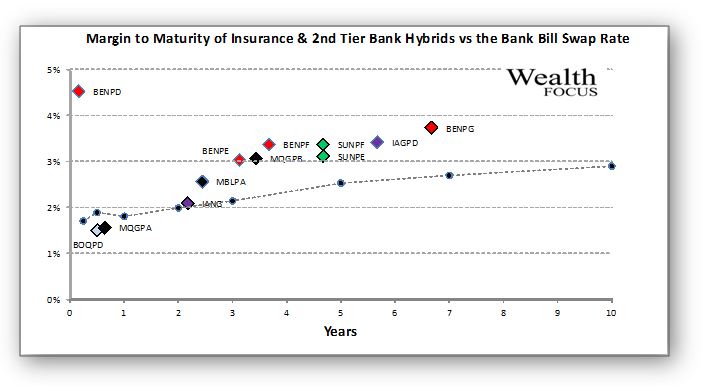

Unlike the Big 4 banks which are arguably different colours of the same entity, the second tier banks each have their own quirks and demand a premium/discount for the relative risks.

One of the primary differentiators is arguably the lack of issuance leading to a tighter trading margin than we would expect among second tier bank and insurance issuers.

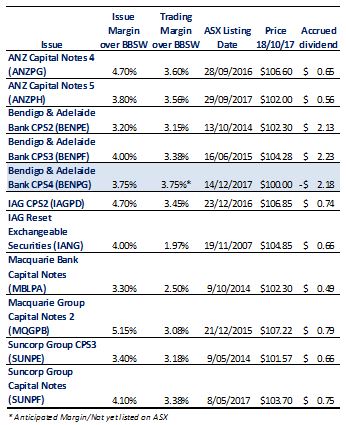

We view ANZ Capital Notes 4 (ANZPG), ANZ Capital Notes 5 (ANZPH) and IAG CPS2 (IAGPD) as the closest comparables, maturing in March 2024 & 2025 and IAGPD in June 2023.

Naturally, Bendigo & Adelaide Bank CPS2 and CPS3 should be considered, but investors should note the considerably shorter anticipated call dates in 2020/2021.

At first glance, BENPG’s margin of 3.75% over BBSW looks to be relatively cheap versus its banking peers, Macquarie, Bank of Queensland and Suncorp Bank, but it is in line with previous issues BENPE and BENPF, that typically trade at a wider margin.

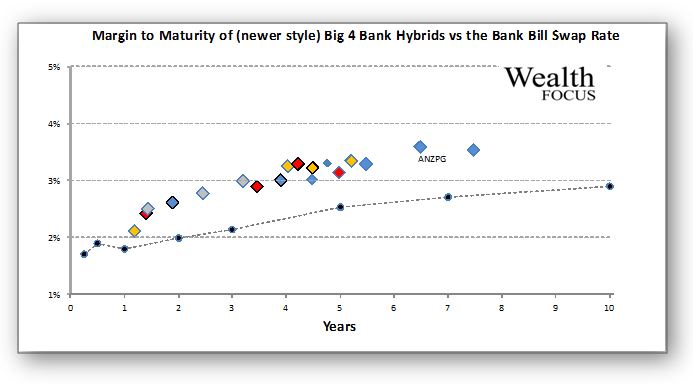

By contrast, the Big 4 bank issuers are trading at similar spreads with arguably less risk and should command a premium of the second tier counterparts. ANZ Capital Notes 4 (ANZPG) is BENPG’s closest comparable and trades at a margin of 3.6% over the BBSW, a difference of only 0.15%pa.

Non-viability Clause, Capital Trigger Event and Inability Event

Investors who are familiar with the new style hybrids we have seen over the last few years will be very aware of these clauses.

It is perhaps useful to understand that these clauses are as a result of APRA requiring further reassurance that in another GFC event, if required, hybrids would convert to ordinary equity, thereby reducing the bank’s debt costs and protecting deposit holders.

Now that banks have to hold a higher level of capital and a better quality loan book, it seems unlikely that any of these conditions would be breached, however, investors would do well to consider the increased disclosure and warnings within each prospectus over the last couple of years.

For those unfamiliar with the conditions, new hybrids now contain non-viability and capital trigger clauses that should the bank’s Tier 1 Capital Ratio fall below 5.125%, or APRA views the bank as non-viable without an injection of capital, the hybrids would automatically convert to ordinary shares.

We have also seen a gradual introduction of an Inability Event Clause added which states that in the event that the issuer is unable to issue further ordinary shares, ie the company has ceased trading, a Capital Trigger Event or Non-Viability Event, hybrid note holders lose their investment.

This is extremely unlikely, but investors would do well to remember the increase in yield offered carries additional risk.

Bendigo & Adelaide Bank CPS (BENPD) Reinvestment Offer

This issue is primarily to refinance BENPD due to be repaid in December this year. Existing BENPD investors have three options:

- Sell BENPD on market before it ceases trading on the 24th November 2017

- Do nothing and the shares will be repaid at $100 per share plus a $2.4041 fully franked dividend

- Participate in the Reinvestment Offer before the 1st December and receive 1 BENPG share for each BENPD held plus $2.4041 fully franked dividend

With BENPD offering an annualised margin to maturity of 4.6% over the BBSW, investors not looking to participate in the reinvestment offer, would do well to consider allowing the shares to be repaid (note: hybrid securities need to be held for 90 days for investors to benefit from the franking credit).

Our view on hybrid margins

Our overall view on hybrid spreads is that they continue to offer relative value to investors. This year has seen a net redemption of hybrids, leading to money returning to the secondary market, further contracting spreads. There is less pressure on the banks to raise their capital ratios and we anticipate the hybrid issuance to continue to contract, and the wider margins still being offered by new issues are likely to be relatively attractive over the coming year.

Our view on Bendigo & Adelaide Bank CPS 4

We are in no doubt that due to the size of the offer and limited issuance this year, Bendigo & Adelaide Bank CPS 4 will be heavily oversubscribed and close early and at the bottom of the indicative range at 3.75% over BBSW.

Relative to alternatives such as ANZPG, we feel investors should demand a premium of close to 4% over the BBSW and BENPG looks expensive if issued at a margin of 3.75%-3.95% (approx 3% overpriced). However, with limited supply and investors looking to diversify their portfolio, we would not be surprised to see this initially trading at par before eventually moving towards a wider margin than its relative peers.

Contact us on 1300 559 869 if you would like an allocation to Bendigo & Adelaide Bank CPS 4 or have an existing investment in Bendigo & Adelaide Bank CPS (BENPD) you would like to roll into the new issue.

Key features

- Indicative floating yield of 5.45%-5.65%pa – based on current 90 BBSW of 1.70% and bookbuild margin range of 3.75%-3.95%.

- Option to redeem at year 6.5 with scheduled conversion at year 8.5 – Bendigo & Adelaide Bank has the option to convert in June 2024 or on any subsequent dividend payment date.

- Ordinary dividend restrictions – applies on the non payment of BENPG dividends

- Automatic conversion under the Capital Trigger Event and Non-Viability

- Redemption highly likely in 6.5 years – although BENPG has a 8.5 year maturity, we view it likely that Bendigo & Adelaide Bank will redeem/convert at the first call date in June 2024. Major incentives for redemption/conversion include the potential for reputational damage and risk of credit rating downgrade, leading to an increased cost of funding on future debt issues.

Note: Bendigo & Adelaide Bank CPS 4 will be listed on the ASX and as such the price of the shares will be subject to market movements. Investors selling on market may receive a price lower (or higher) than the issue price.

Find out more

If you would like further information on Bendigo & Adelaide Bank CPS4 Offer, please click on the links below:

Investors looking for an allocation can contact us on 1300 559 869

We encourage you to view our online presentation An Introduction to Fixed Income

Comments | Click to comment

Dear Sir,

We have read with interest your analysis of the BENPD – CPS4 (BENPG) offer.

In this regard, we contacted Bendigo’s registry last week and they confirmed that there is also a 4th option, to convert the BENPD to BEN ordinary shares, over and above the three options you have stated in your review. This is not disclosed in any of the preliminary summaries provided to the market in recent weeks (and they admitted this serious omission). We believe many BENPD shareholders will miss this very useful 4th option. They also advised that the final BENPD dividend would be paid if the offer to convert to ordinary shares is requested. This 4th option is a useful one, because it means that one can simply convert BENPD to ordinary shares without having to pay brokerage. This omittance should be explained in your assessment of the BENPD – BENPG offer.

David Amstell

David, 23 October, 2017

Hi David

I would be surprised if they allowed the 4th option to convert into ordinary shares as it would be at a 2.5% discount and would dilute existing shareholders. I note that the BENPD prospectus (page 7) states these are the conditions at Mandatory Conversion in Dec 19, but the Optional Exchange conditions differ.

They state that “Exchange means:

If they did offer this, it would most certainly be worthwhile.

I have not heard this from any of the brokers we deal with, so I suspect the registry has misinformed you

Sulieman Ravell, 23 October, 2017

Comment: